New to Loans? Here is your guide to What CIBIL Means and Why Banks Care About It?

Learn what a CIBIL score is, how it impacts home loan approvals, interest rates, and loan eligibility in India, and smart ways to build and improve your credit score in 2026.

Contents

Imagine you walk into a bank to fulfil a life-long dream- buying your first home or starting a business. You’ve got the down payment ready but the bank manager looks at a screen and says, "Sorry, your CIBIL score is too low."

For many Indians, this is where the dream hits a roadblock. If you’ve never heard of CIBIL, don’t worry-you aren’t alone. But in 2026, understanding this number is just as important as knowing your bank account balance.

What exactly is a CIBIL Score?

If you are new to the world of finance, think of CIBIL as your Financial Identity Card.CIBIL stands for Credit Information Bureau (India) Limited. It is India’s first and most trusted credit bureau. It collects data from all banks and financial institutions about how you manage your money.

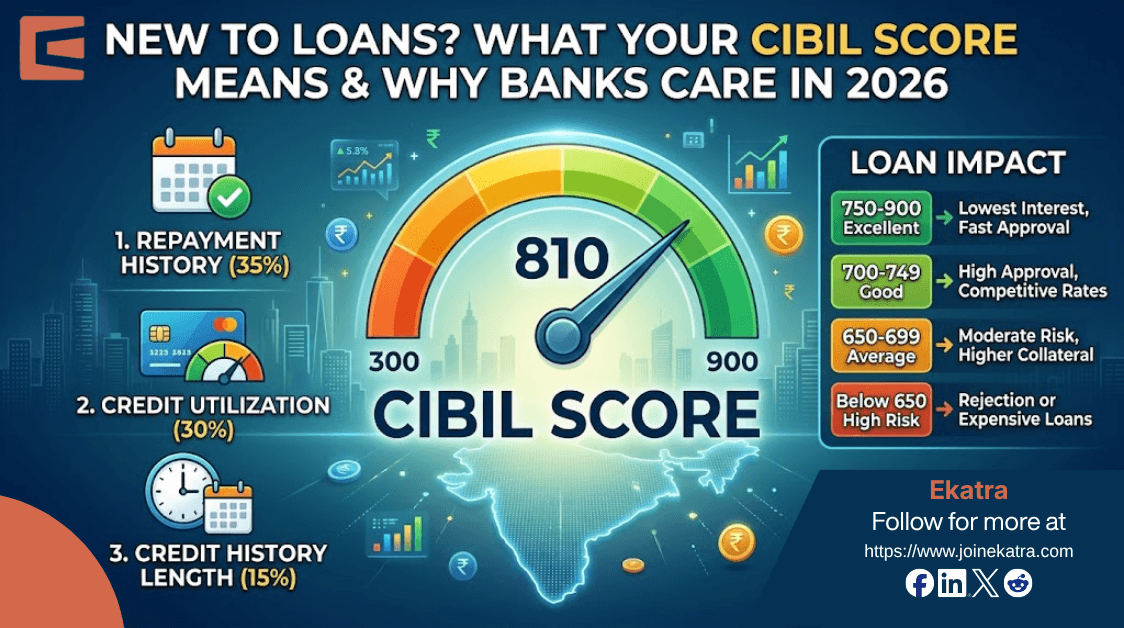

Based on your credit history-your past loans, credit card usage, and repayment patternsCIBIL gives you a score between 300 and 900.

Essentially, your CIBIL score tells a lender "Is this person responsible? If I lend them ₹10 Lakhs, will they pay it back on time?"

The 2026 CIBIL Scorecard: Where Do You Stand?

In India’s rapidly evolving digital economy, lenders are more data-driven than ever. Your score dictates how much you'll pay in interest and how fast you can get approved.

| Score Range | Category | Loan Impact |

| 750-900 | Excellent | Instant approvals, lowest interest rates |

| 700-749 | Good | High approval chances, competitive rates |

| 650-699 | Average | Moderate risk, lenders may ask for higher collateral or interest |

| Below 650 | High Risk | High chance of rejection or very expensive loans |

How Your CIBIL Score Directly Impacts Your Wallet

Recent market research in 2026 shows that lenders are moving toward "Risk-Based Pricing." This means two people applying for the same ₹10 Lakh loan could pay vastly different amounts based purely on their scores.

- Interest Rates: The "Credit Discount"

A score of 800+ can save you lakhs of rupees over a 20-year home loan. Lenders view high-score borrowers as low-risk and offer them "Prime" interest rates. Conversely, if your score is below 700, you might be charged a 2-4% premium, which adds up significantly over time.

- Faster Approvals & Higher Loan Amounts

In 2026, many Indian banks use automated AI-driven systems for loan processing. If your score is above 750, you might get a "pre-approved" offer with zero documentation. A high score also gives you the leverage to negotiate for a higher loan-to-value (LTV) ratio.

- The "Credit Mix" Factor

Lenders now place higher value on a healthy "Credit Mix"—a balance of secured loans (like a car or home loan) and unsecured loans (like credit cards). Showing you can manage both types of debt boosts your credibility.

Top 5 Factors That Move Your Score in 2026

According to current financial trends, these factors carry the most weight:

1.Repayment History (35%): Even a single late payment on a credit card or EMI can cause a 50-point dip.

2.Credit Utilization (30%): Using more than 30% of your total credit card limit signals "credit hunger."

3.Credit History Length (15%): Older accounts prove stability. Don't close that 10-year-old credit card!

4.Hard Inquiries: Every time you apply for a loan, a "hard inquiry" is made. Multiple inquiries in a short period can lower your score.

5.Report Accuracy: With real-time reporting now the standard, a single reporting error by a bank can haunt your score. Always check your report for mistakes.

Zero Credit History? Here’s How to Start

If you’ve never taken a loan, your score might show as "NA" or "-1". This isn't bad, but it makes it hard for banks to judge you.

The Fix? Get a "Secured Credit Card" against a small Fixed Deposit (FD). Use it for small purchases and pay it back in full every month. Within 6 to 8 months, you will have a shining CIBIL score!

In the India of 2026, your CIBIL score is your most valuable financial asset. It’s not just about getting a loan; it’s about getting it on your terms. In conclusion, treat your score like you treat your reputation.

The GOLDEN RULE is to pay on time, keep your debt low, and check your CIBIL report at least once a year to ensure there are no errors. Your future self (and your bank account) will thank you!

Written by

Ananya Das